Buffet's Bet

The primary purpose of a hedge fund is to minimize draw-downs during market corrections/crashes - hence the word “hedge” in the name. A lot of people don’t seem to understand this.

The reason is because qualified investor goals are not returns against the market. But returns against inflation while minimizing draw-downs. It’s a dual mandate.

Most wealthy people accrue wealth primarily via other means.

In 2005, Warren Buffet famously made a $1 million wager (really he wagered $500k) that no fund manager could beat the S&P in returns over a decade - or at least that is the version of this wager that gets repeated.

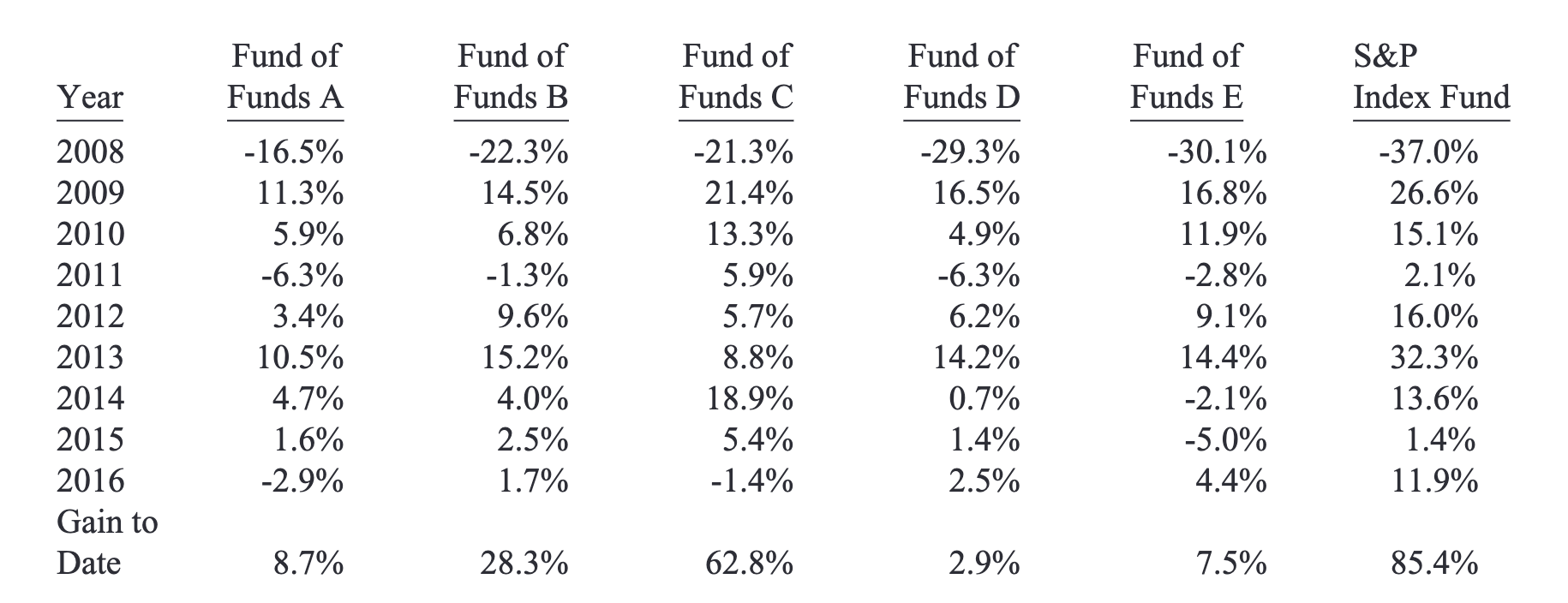

Here is the result of that wager. Vanguard’s S&P 500 index fund soundly beat the basket of hedge funds. End of story.

No need to read further.

Just what are the odds of the stock market having 8 consecutive years without falling by more than 10%? The conditions that happened to unfold post 2008.

Since 1927, 34 out of 93 (36.6%) of all 8-year periods had no single year with a return worse than -10%. Which means this period was an anomaly in market history.

Over that same period, 12% of years had a return worse than -10%. Since no one can see the future but we can see the past. How would that wager have worked out during the 2/3rds of market history where there was a second year in that decade with a draw-down of 10%?

Using the returns state above we can estimate. If that 10% return fell during 2012, 2013 or 2016, Fund of Funds C would have beaten the index. So 30% of the time a basket of hedge funds would have beaten the index while not taking as severe a draw-down.

What if there was a draw-down greater than 20%? Which over the time period occurs in 6% of years? If that draw-down fell in 2009, 2012, 2013, or 2016, Fund of Funds C would have beaten the index 40% of the time.

No one could have predicted quantitive easing would go on for 14 years in 2005 when Buffet offered his bet. At the time during historically predictable and expected market conditions Fund of Funds C would have accomplished it’s goal of minimizing draw-downs AND beaten the index between 30-40% of the time.

Is that great odds? Not really.

But remember, only qualified/accredited investors can invest in hedge funds and our goals are not the same as yours. Qualified/accredited investors aren’t saving for an early retirement. This class of investors just want stable returns without significant draw-downs. Just like you don’t want the appraised value of your house to fall 50% after you take out a home equity loan requiring you to give the bank more collateral.

What people take away from Buffet’s bet is that a retail investor is better off in an index fund. This is not necessarily true on two accounts. First, as stated, retail don’t have the option of a hedge fund. A retail investors options are buy an index and ride, buy an index and try to hedge yourself and under perform the index, or actively manage your own account.

This is one problem of comparing your situation to the situation of people who are investing in hedge funds.

And second, most people don’t realize that Buffet’s criteria was comparing unhedged indexing vs hedged indexing - Vanguard’s S&P 500 index is not hedged - not test active management vs. passive management.

Here is Buffet:

"... no investment pro could select a set of at least five hedge funds – wildly-popular and high-fee investing vehicles – that would over an extended period match the performance of an unmanaged S&P-500 index fund charging only token fees..."What people take away from Buffet’s bet is that active investors can’t beat the S&P so they (retail investors) are better off investing in a passive index.

This is absolutely false.

If you had just bought the top 5 stocks in the S&P 500 over the last decade you would have beaten the S&P 500 and not had to pay Vanguard a management fee. You can check my math there if you want. More on this in a minute.

But, the side of Wall Street that collects fees from managing index funds loves to repeat dubious result.

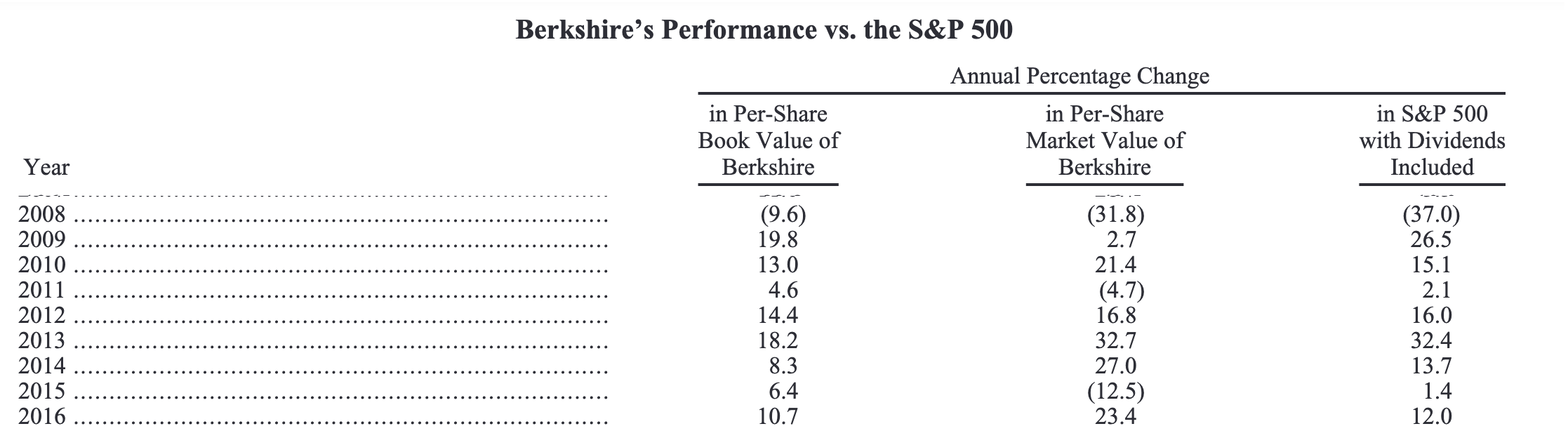

On another note, it’s curious that Buffet didn’t put Berkshire Hathaway’s returns over the same period of the wager. In case you were wondering, Berkshire Hathaway from 2008-2016 did have a second year with a draw-down of more than 10%. In 2015, Buffet lost -12.5%. Here are Berkshire’s returns from his investor letter.

I will leave the math to you to see how Berkshire did compared to both Vanguard and to the various Fund of Funds. You probably don’t need a calculator to know the answer there.

The former hedge fund manager, Bill Hwang, turned $200 million into $20 billion over the time period of 2013 to 2021 which is a CAGR if 78%. The S&P returned ~16% during this time period.

So “active management” can easily out perform indexing. Bill Hwang then of course lost it all over a two day period in 2021 because he wasn’t properly hedged.

So don’t forget to hedge. Nor forget why people pay fees to managers who are good at hedging.

-AJ