Business Development Corporations (BDCs)

Friday March 13, 2026

Some history of BDCs.

Allied Capital Corp went IPO in 1960. From 1960 until 2001 it was OTC but went public in 2001 were it was immediately hit with turbulence in the name of David Einhorn who alleged Allied Capital was inflating its marks. Going so far to say its subsidiary Business Loan Express was an outright fraud. So Allied Capital changed the name of Business Loan Express to Cienna Capital in the hopes to save the stock price. It might have worked had Einhorn been wrong and Cienna not declared bankruptcy. In 2002, Allied Capital was trading at ~$25.80/share. By April of 2009, it was trading at $2.50. The rope ran out. When Cienna filed for bankruptcy Allied was down 50% already.

Eventually, Allied Capital was acquired by Ares Capital for $3.47 per-share. Under the deal, Allied Capital shareholders received 0.325 Ares Capital shares for each share held.

Ares Capital is still around. The transacted shares as of today (ignoring dividends) are up 96% in 16 years. Ares is currently trading right at NAV.

Electra Investment Trust is out of the UK. Trust companies are not very common in the US market the reason (I think) has to do with voting rights. Electra Investment Trust was formerly deleted from the London Stock Exchange in 2024 after forming a triple black diamond slope.

Candover Investments was founded in 1980 and was gone by 2008.

3i Group has a long history in the UK. It is basically a locked float. It owns things like the Belfast Airport. It is trading roughly at NAV as well today after falling 30% since November.

SVG Capital went defunct in 2017.

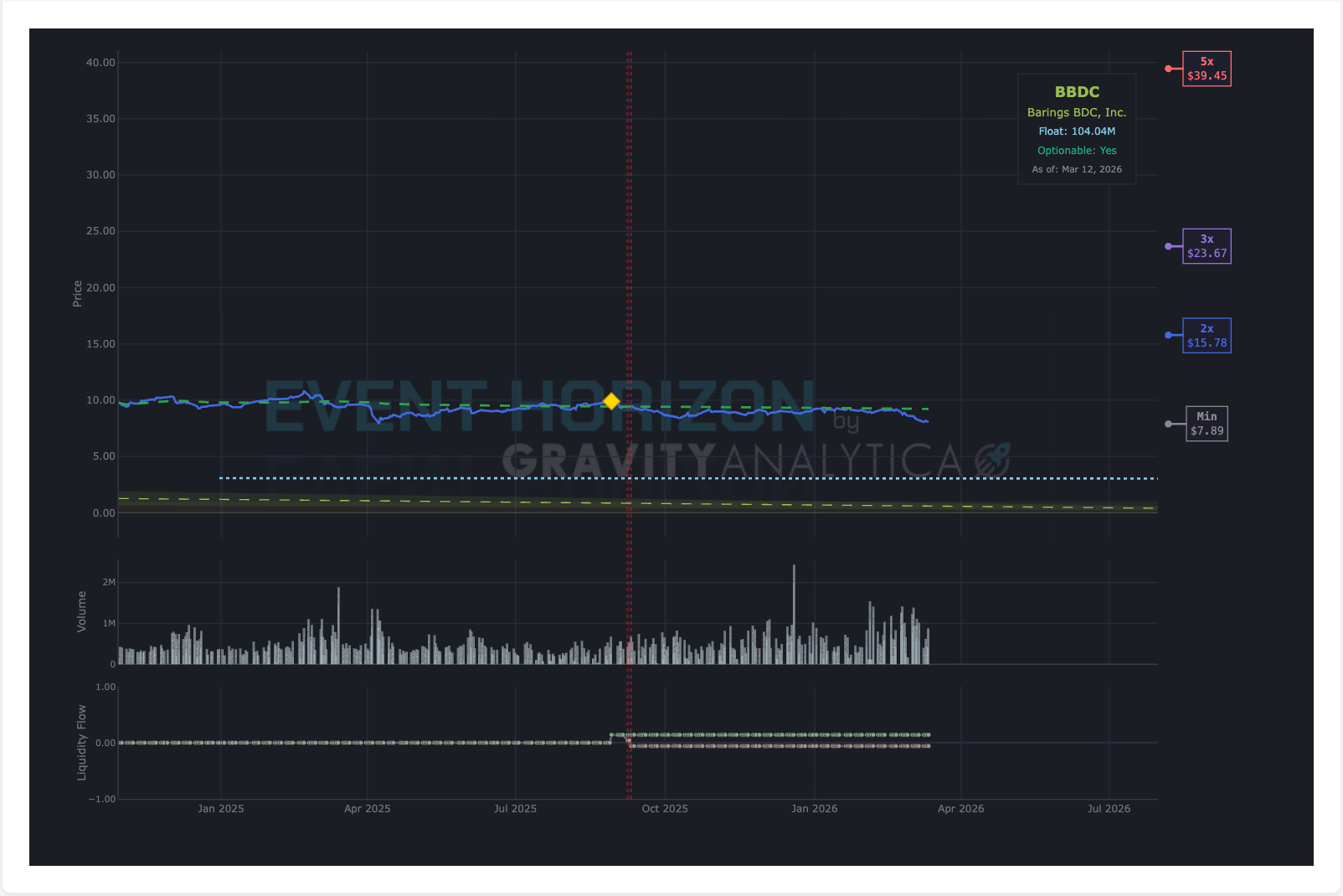

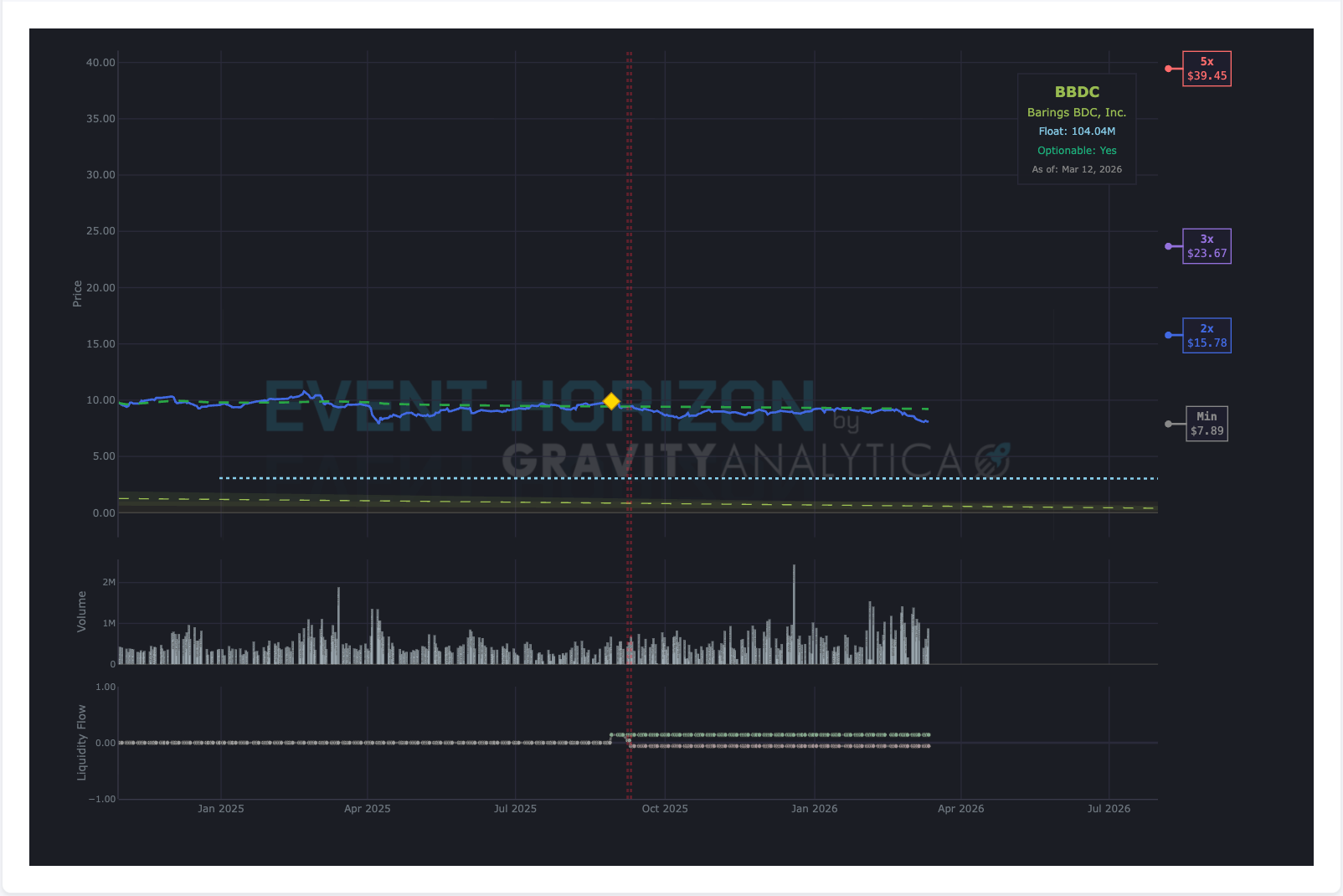

MVC Capital was acquired by Barings BDC in 2020 for $10/share (basically MVC Capital share holders got one share of Barings BDC) and guess what? That’s where it’s traded since.

Apollo Investments Corp now MidCap Financial…

I don’t want to waste your time reading about every BDC in the market history. But, there is nothing about the new class of BDCs that makes them special to the grandfathers above. BDCs are not wealth creation engines and never have been.

What is important is that these companies only trade above NAV when there is market euphoria and just too much capital. Rising tide lifts all boats. Trading at 70% NAV is normal.

BDCs are much more likely to contain toxic or potentially toxic assets than they let on to. Remember, the public sector is where smart money dumps assets that are too risky.

That means no BDC will ever be evaluated (correctly) at or above NAV. If a company is seem as a safe bet with growth prospects it won’t be held in any public vessel.

So even before AI was a problem BDCs should not have traded anywhere near as high as they were in late 2025. The current evaluations just reflect “normal” not “distressed.”

You haven’t seen distressed yet. During the last credit crunch BDCs traded at an average of 30% NAV. Are we in a credit crunch now? The last credit crunch started with a surge in oil as well. I already did the comparison of today to the GFC.

Remember, the securities are riding an escalator to nowhere and the public sector is the last line to get off.

In order of value to risk you have single owner, family owned, privately securitized, publicly securitized.

OnlyFans which generates a lot of profit and has no debt, is owned by one guy. Chick Fil A is owned by one family. The public sector is where stocks go to die.

And occasionally do something unexpected. But mostly, die.

Great companies don’t need to go public. Great investments don’t need to be chopped up into a BDC either.

We have no investments in BDCs. Though we do operate in the PC/PE space.

As always, if you think there are spelling errors update your dictionary to the latest version. Happy speculation!

— AJ